2026 State of Digital Manufacturing Report: Small & Midsized Companies in the United States

Research & analysis from our Q1 2026 survey of U.S. small and mid-sized manufacturers examining the adoption, priorities, and challenges of digital manufacturing.

The landscape of digital manufacturing in the United States is evolving rapidly, and small- to medium-sized manufacturers (SMBs) are at a pivotal crossroads. As global competition intensifies and customer demands shift toward greater customization, speed, and quality, digital technologies—from advanced automation and additive manufacturing to cloud-based analytics and IoT-enabled machinery—are no longer optional enhancements but strategic imperatives. This report provides a comprehensive assessment of the current state of digital manufacturing adoption among U.S. SMB manufacturers, highlighting key trends, opportunities, challenges, and actionable insights to help manufacturers modernize operations, enhance competitiveness, and drive sustainable growth in an increasingly digitized economy.

This report was compiled by surveying SMB manufacturers in Q1 2026 across 14 manufacturing industry sectors and sizes, with 84% of respondents being from manufacturing companies with less than 1000 employees. Survey responses were used to assess various aspects of digital adoption including self-assessed levels of adoption and ROI.

Contents

Current state of digital adoption across manufacturing & supply chain operations

Current state of data & analytics in manufacturing & supply chain operations

ROI Ratings on Recent Digital Investments

Operational Improvements Gained from Digital Investments

Highest priority near-term operational digital investment areas

Highest priority near-term technology investment areas

Confidence in ability to achieve ROI from digital investments

Barriers to digital manufacturing initiatives

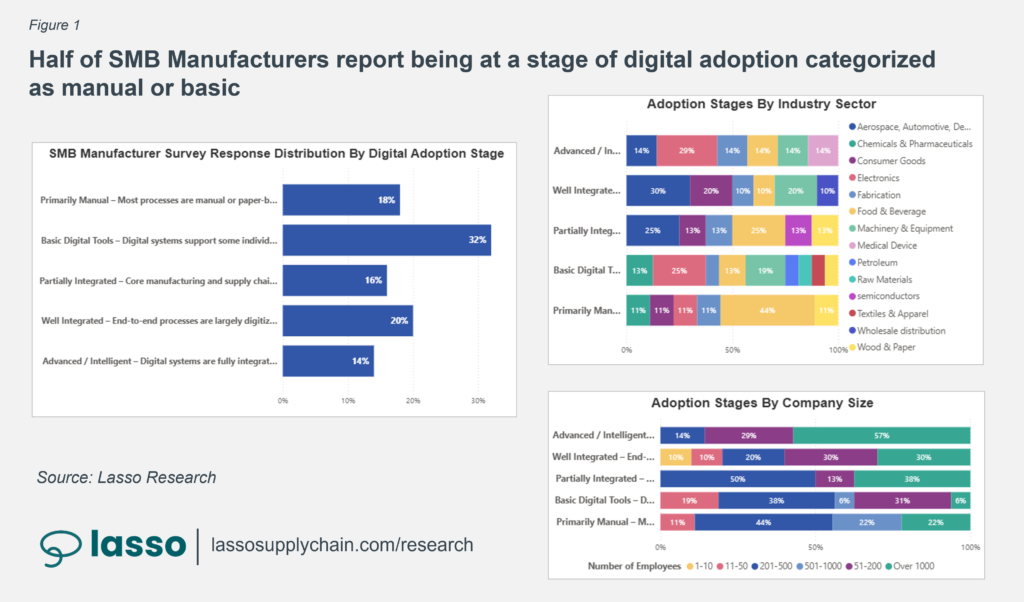

Current state of digital adoption across manufacturing & supply chain operations

Digital adoption across manufacturing and supply chain operations has accelerated in recent years, yet progress remains uneven across functions, technologies, and company sizes. While many organizations have invested in ERP upgrades, automation, and data visualization tools, fewer have achieved true integration across production, inventory, procurement, logistics, and planning. As a result, critical decisions are still often made with fragmented data, manual workarounds, and limited real-time visibility. This section examines the current maturity of digital capabilities across core operational areas, highlighting where adoption is gaining traction, where gaps persist, and what these patterns signal for the next phase of digital transformation in manufacturing.

Insights at a Glance: State of digital adoption in manufacturing

- Around 50% of surveyed SMB manufacturers assess their level of digital adoption as being at a level of manual processes or some basic digital tools.

- Among those surveyed self-assessing at above a level of basic adoption (partially integrated, well integrated, and advanced), 8% were companies with under 50 employees.

- Wholesale distribution & Aerospace, Automotive, & Defense sectors had the highest level of digital adoption, scoring 4.0 & 3.8 respectively (on a 5-point scale).

- 100% of wholesale distribution & aerospace/automative/defense sectors rated themselves at above a level of basic digital adoption and as having some level of integration.

- Chemicals, Wood Products, and Textiles had the lowest stated adoptions, scoring 1.7, 2.0, and 2.0 respectively. 60% reported being at a level of having primarily manual processes without digital workflows.

Manufacturing’s digital divide is widening, with integration—not adoption—emerging as the true competitive differentiator.

The data underscores a widening digital maturity gap across the manufacturing landscape. While adoption has clearly accelerated, the reality is that for roughly half of SMB manufacturers, digital operations remain limited to spreadsheets, siloed systems, and incremental tool deployments rather than fully integrated workflows. This suggests that “digital transformation” for many firms is still tactical rather than strategic — focused on solving immediate pain points instead of building an interconnected operational backbone.

The size-based disparity is particularly notable. With only 8% of companies under 50 employees reporting adoption beyond basic levels, smaller manufacturers appear constrained not just by capital, but by bandwidth, expertise, and organizational readiness. For these firms, digital transformation competes directly with day-to-day operational demands. Without clear ROI pathways and implementation support, many remain in a holding pattern of partial digitization.

Sector variation further illustrates how market forces shape digital maturity. Industries such as wholesale distribution and aerospace/automotive/defense — often characterized by higher regulatory requirements, tighter margins, complex supply chains, and demanding customers — have stronger incentives to invest in integration and visibility. Their higher maturity scores suggest that external pressure, customer expectations, and supply chain complexity accelerate digital adoption. In contrast, sectors like chemicals, wood products, and textiles, where processes may be more stable or less customer-driven by real-time data requirements, show significantly lower adoption levels and higher reliance on manual workflows.

Looking forward, several implications emerge:

- Integration will define the next competitive divide.

The next phase of digital transformation will not be about adding more tools, but about connecting existing systems — linking ERP, MES, inventory, procurement, and planning into unified data environments. Organizations that move from functional digitization to end-to-end integration will unlock better forecasting accuracy, improved inventory turns, and stronger margin control. - SMB enablement will be critical.

Technology providers and service partners must simplify pathways to value for smaller manufacturers. Modular, phased implementation models and clearer ROI narratives will be essential to prevent smaller firms from falling further behind digitally mature competitors. - Industry-specific digital roadmaps will matter more.

Adoption patterns suggest that a one-size-fits-all digital strategy is ineffective. Sector-specific pressures — compliance, traceability, customization, or supply volatility — will increasingly dictate digital investment priorities. - Talent and data literacy will become binding constraints.

Even as tools become more accessible, organizations will need stronger internal capabilities to interpret and act on operational data. The competitive advantage will shift from owning software to operationalizing insight.

Ultimately, the survey findings indicate that manufacturing is at an inflection point. The foundational technologies are widely available, but the differentiator over the next 3–5 years will be execution: who can integrate systems, align digital initiatives to measurable operational outcomes, and embed data-driven decision-making into everyday workflows. Those that do will likely see gains in resilience, cost control, and customer responsiveness — while those that remain reliant on fragmented or manual processes risk widening performance gaps in an increasingly data-driven supply chain environment.

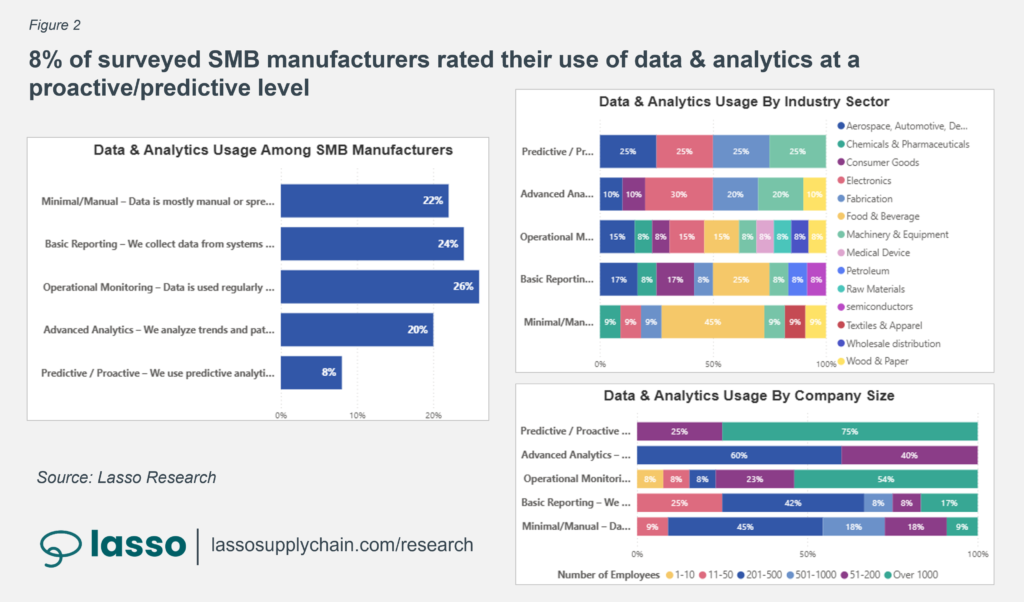

Current state of data & analytics in manufacturing & supply chain operations

Data and analytics have become central to operational performance in manufacturing and supply chain environments, yet maturity levels vary widely across organizations. While most manufacturers now capture significant volumes of production, quality, inventory, and logistics data, far fewer consistently translate that information into timely, decision-grade insights. Many operations remain constrained by siloed systems, inconsistent data governance, and limited advanced analytics capabilities, resulting in reactive decision-making rather than predictive or prescriptive optimization. This section examines the current state of data infrastructure, reporting practices, analytics adoption, and organizational capabilities shaping how manufacturers leverage data to improve efficiency, resilience, and profitability across the value chain.

Insights at a glance: State of data & analytics in manufacturing

- 46% of surveyed SMB manufacturers rated their use of data & analytics at a manual or basic level.

- 26% of respondents rated themselves as regularly using analytics in operational monitoring to track performance & identify issues.

- 20% used analytics to identify trends and patterns to improve their planning, forecasting, or process optimization.

- 8% of surveyed SMB manufacturers used it for predictive modeling. 75% of organizations that used predictive models had over 1,000 employees.

- 80% of companies under 50 employees reported being at a manual or basic level.

- Despite having a high level of digital adoption, 71% of wholesale distribution and aerospace/automative/defense report being at a basic or operational monitoring level. 29% report being at an advanced, predictive level.

- Electronic manufacturing reported the highest level of analytics utilization, scoring 3.4 (on a 5-point scale). Textiles reported the lowest at 1.0.

Manufacturers are data-rich but insight-poor, with predictive analytics concentrated among the largest enterprises.

The findings reveal a clear imbalance between data availability and analytical maturity. While most manufacturers are generating significant operational data, nearly half of SMB respondents remain at a manual or basic level of analytics usage. This indicates that data capture has outpaced data utilization. Dashboards may exist, reports may be generated, but decision-making in many organizations is still reactive and backward-looking.

The sharp drop-off from operational monitoring (26%) to trend-based optimization (20%) and especially to predictive modeling (8%) highlights how steep the maturity curve remains. Predictive capabilities — often considered a hallmark of advanced operations — are overwhelmingly concentrated in large enterprises, with 75% of predictive adopters employing more than 1,000 people. This signals that advanced analytics adoption is strongly correlated with organizational scale, technical resources, and dedicated data teams.

The size-based disparity is even more pronounced among smaller firms: 80% of companies under 50 employees report operating at a manual or basic level. This suggests that for the smallest manufacturers, analytics is still largely descriptive, if not spreadsheet-driven.

Sector differences add another layer of nuance. Even industries such as wholesale distribution and aerospace/automotive/defense — which previously showed strong digital adoption — report that 71% remain at a basic or operational monitoring level in analytics maturity. This indicates that digital system deployment does not automatically translate into advanced analytical capability. By contrast, electronic manufacturing, with the highest analytics score (3.4), likely benefits from tighter quality requirements, shorter product cycles, and higher data intensity, all of which create stronger incentives for advanced analytics. At the opposite end, textiles’ low score (1.0) suggests limited integration of analytics into core operational decision-making.

Overall, the pattern suggests that many organizations have built digital infrastructure but have not yet operationalized analytics as a strategic capability.

Forward-Looking Implications

- The next leap is from visibility to foresight.

The competitive advantage will shift from tracking KPIs to anticipating outcomes. Organizations that move into predictive and eventually prescriptive analytics will gain earlier signals on demand shifts, quality risks, capacity constraints, and supplier performance. - Talent and governance will matter more than tools.

Technology is increasingly accessible, but sustainable analytics maturity requires data governance, standardized metrics, and internal capability development. Firms that invest in data literacy and cross-functional ownership of analytics will outperform those that treat analytics as a reporting function. - SMBs need simplified pathways to advanced analytics.

The concentration of predictive modeling in large enterprises suggests a widening capability gap. Cloud-based platforms, embedded AI features in ERP systems, and external analytics partnerships may become critical accelerators for smaller manufacturers seeking to compete without building large internal teams. - Integration does not equal optimization.

Even digitally mature industries demonstrate limited advanced analytics penetration. The next transformation wave will require turning integrated data into embedded decision engines that influence scheduling, inventory policy, procurement strategy, and pricing in real time. - Industry-specific use cases will drive adoption.

Sectors with high product complexity, regulatory scrutiny, or demand volatility are likely to lead the predictive shift. Others may follow as margin pressure and supply chain variability intensify.

In summary, manufacturing is transitioning from a phase of digitization to one of analytical enablement. The organizations that successfully evolve from descriptive reporting to predictive insight — and ultimately prescriptive action — will define the next generation of operational excellence.

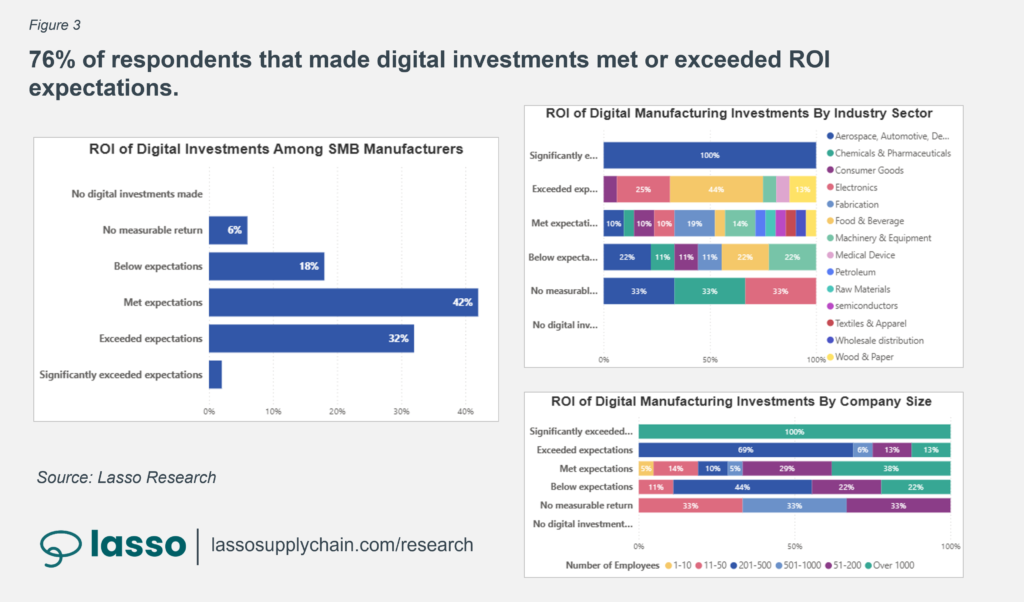

ROI Ratings on recent digital initiatives

As digital investments accelerate across manufacturing and supply chain operations, executive teams are increasingly focused on measurable returns. While many organizations have deployed new technologies—ranging from automation and IoT to advanced analytics and cloud platforms—the realized value varies significantly by initiative, execution maturity, and alignment with business objectives. In some cases, projects have delivered clear gains in productivity, cost reduction, and visibility; in others, benefits have fallen short of expectations due to integration challenges, change management gaps, or unclear performance metrics. This section evaluates how manufacturers are rating the return on investment (ROI) of recent digital initiatives, highlighting patterns in realized value, time-to-impact, and the factors that most strongly influence successful outcomes.

Insights at a glance: Digital Investment ROI

- 76% of respondents that made digital investments met or exceeded ROI expectations.

- Companies with over 200 employees reported the highest ROI score on recent investments, at 3.4 (on a 5-point scale).

- The chemicals manufacturing industry had the lowest reported recent ROI score at 1.7 (out of 5).

- Medical device manufacturing had the highest reported ROI score at 4.0 out of 5.

Most digital investments are delivering returns—but scale, industry dynamics, and execution maturity determine the magnitude of impact.

The findings suggest that digital investment skepticism is increasingly giving way to measurable results. With 76% of respondents reporting that they met or exceeded ROI expectations, the broader narrative is one of cautious validation: digital initiatives, when executed effectively, are generating tangible operational and financial benefits.

However, ROI outcomes are not evenly distributed. Larger organizations — particularly those with over 200 employees — reported the highest average ROI scores (3.4 out of 5). Scale likely provides structural advantages: deeper implementation resources, stronger change management capabilities, more standardized processes, and the ability to spread fixed technology costs across larger revenue bases.

Industry variation is equally revealing. Medical device manufacturers reported the highest ROI (4.0), while chemicals manufacturing reported the lowest (1.7). Highly regulated, quality-intensive industries such as medical devices often operate with tighter traceability, compliance, and performance requirements, creating clearer value pathways for digital investments. In contrast, industries with complex legacy processes, capital intensity, or longer production cycles may face slower realization timelines or integration challenges that dampen near-term ROI.

Importantly, the relatively strong ROI ratings across most respondents suggest that the primary risk is no longer whether digital investments can pay off — but whether organizations can execute them effectively and consistently.

Forward-Looking Implications

- Execution capability will become the primary ROI differentiator.

As adoption increases, the competitive gap will shift from who invests to who implements effectively. Integration discipline, leadership alignment, and change management will drive realized value more than the technology itself. - Smaller firms must be precise in prioritization.

While larger companies may absorb missteps, smaller manufacturers will need sharper use-case selection, faster time-to-value initiatives, and clearly defined performance metrics to replicate strong ROI outcomes. - Industry context shapes value realization speed.

Highly regulated or quality-sensitive sectors may continue to lead in ROI performance due to stronger alignment between digital capabilities and operational risk mitigation. Other sectors may require longer-term investment horizons. - ROI expectations will rise.

As more companies report positive returns, executive teams and boards will increasingly expect digital initiatives to demonstrate quantifiable business impact — shifting conversations from experimentation to accountability. - The focus will move from project-level ROI to portfolio-level value creation.

Leading manufacturers will begin measuring digital ROI not as isolated initiatives, but as interconnected investments that compound benefits across planning, production, inventory, and customer service.

In sum, digital investments in manufacturing are proving their economic case. The next phase will require disciplined scaling — turning successful pilots into enterprise-wide capability while maintaining measurable, repeatable returns.

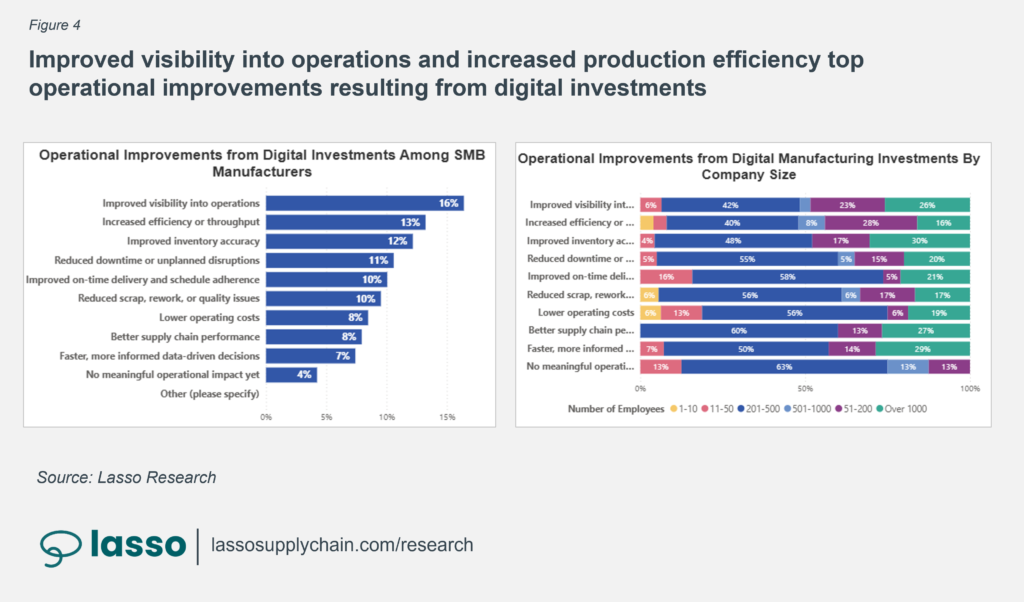

Operational Improvements Gained from Digital Investments

Digital investments across manufacturing and supply chain operations are increasingly evaluated not just by implementation milestones, but by tangible operational outcomes. From improved throughput and reduced scrap to enhanced schedule adherence and inventory optimization, organizations are seeking measurable performance gains tied directly to technology adoption. However, the scale and sustainability of these improvements vary based on data integration, workforce adoption, and process alignment. This section explores the specific operational enhancements manufacturers report achieving through digital initiatives, quantifying where gains are most pronounced and identifying the practices that translate technology investments into durable performance improvements.

Insights at a Glance: Operational Gains from Digital Investments

- Improved visibility into operations was the highest reported benefit (16% of respondents) followed by Increase efficiency/throughput (13%), and Improved inventory accuracy (12%)

- Among the improved visibility into operations category, 61% were from the food & beverage, Electronics, and Machinery Equipment sectors.

- Among respondents with 50 or fewer employees, the top operational gains reported were improved on-time delivery and schedule adherence (25%) and lower operating costs (17%).

- Among firms with 500 or more employees, inventory accuracy, visibility into operations, and increased productivity throughput were the top operational areas cited.

Digital investments are delivering measurable operational gains, with visibility emerging as the foundation for broader performance improvements.

The data indicates that the most immediate and universal benefit of digital investment is improved visibility into operations. As the top reported gain (16%), enhanced visibility suggests that many organizations are first unlocking transparency — real-time production status, inventory levels, and performance metrics — before realizing deeper optimization outcomes.

Efficiency and throughput gains (13%), along with improved inventory accuracy (12%), follow closely behind. This sequencing is important: visibility often precedes productivity. Organizations must first see bottlenecks, material imbalances, and process variation before they can systematically reduce them.

Sector concentration within the visibility category — particularly among food & beverage, electronics, and machinery equipment — suggests that industries with higher production variability, regulatory requirements, or product complexity may derive faster benefits from digital transparency.

Company size again plays a defining role in how value manifests. Among firms with 50 or fewer employees, operational gains skew toward improved on-time delivery and schedule adherence (25%) and lower operating costs (17%). For smaller manufacturers, digital tools appear to directly stabilize execution and reduce day-to-day firefighting. In contrast, firms with 500+ employees cite inventory accuracy, operational visibility, and throughput productivity as primary benefits — improvements that reflect scale-driven optimization and network complexity.

Collectively, the findings suggest that digital investments are not producing uniform outcomes; instead, value realization aligns closely with organizational maturity, complexity, and immediate operational pain points.

Forward-Looking Implications

- Visibility is the gateway to optimization.

Real-time transparency will continue to be the first and most critical step in digital transformation. Organizations that layer analytics and automation on top of improved visibility will generate compounding returns. - Smaller firms prioritize execution stability.

For SMBs, digital success will increasingly be measured by predictable delivery performance and cost control rather than advanced automation. Vendors and service providers must align solutions to these immediate priorities. - Larger enterprises will focus on systemic optimization.

As scale increases, the focus shifts toward network-wide inventory optimization, cross-site coordination, and throughput maximization. Integration across facilities and supply nodes will become a competitive advantage. - Sector-specific operational drivers will shape ROI narratives.

Industries with perishable goods, high customization, or regulatory oversight may continue to see faster operational payback from digital visibility and traceability tools. - Sustainable gains require process alignment, not just tools.

The variability in reported improvements underscores that technology alone does not guarantee durable results. Workforce adoption, standardized workflows, and clear accountability mechanisms will determine whether initial gains persist.

In summary, digital investments are producing tangible operational improvements, particularly in visibility and execution reliability. The next stage of value creation will depend on how effectively manufacturers convert that visibility into predictive, automated, and continuously optimized performance systems.

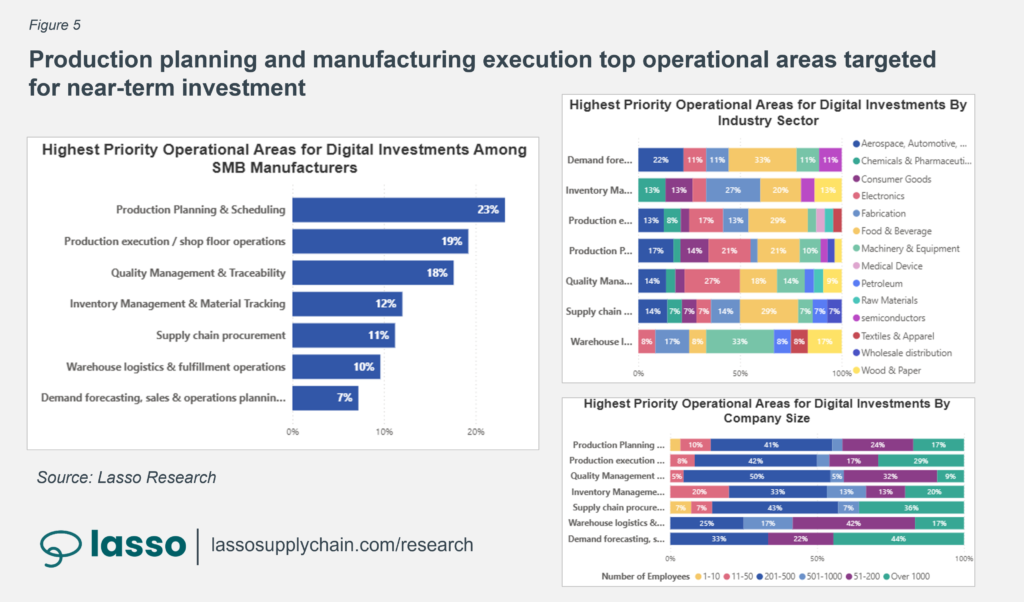

Highest priority near-term operational digital investment areas

As manufacturers navigate economic uncertainty, labor constraints, and rising customer expectations, digital investment decisions are becoming more targeted and outcome-driven. Rather than broad transformation agendas, many organizations are prioritizing focused initiatives that deliver measurable operational impact within the next 12 to 24 months. Areas such as production visibility, inventory optimization, predictive maintenance, supply chain resilience, and advanced analytics are emerging as top contenders for near-term funding. This section examines the digital capabilities manufacturers identify as their highest operational priorities, highlighting where capital and leadership attention are concentrated—and why these areas are viewed as critical to sustaining competitiveness in the current environment.

Insights at a Glance: Near-Term Operations Areas for Digital Investment

- Production Planning and Manufacturing execution were the top operational areas targeted for near-term investment at 23% and 19% respectively.

- Among companies with 200 or fewer employees, production planning & scheduling was the top investment area.

- Among companies with 500 or more employees, manufacturing execution and inventory management were the top priorities for digital investment.

- For Production planning & scheduling, Electronics, Food & Beverage, and Aerospace/Automotive/Defense were the top sectors cited at 21%, 21%, and 17% respectively.

- For Inventory Management, 47% were from Food & Beverage and Fabrication.

- For Quality Management, the Electronics section was the top industry sector at 27%

- For warehousing, logistics, and fulfillment operations, the Raw Material sector was the top sector cited at 33%

Near-term digital investments are converging on production control and execution stability as manufacturers prioritize speed-to-impact initiatives.

The survey findings indicate a clear shift from broad digital ambition to focused operational execution. Production planning (23%) and manufacturing execution (19%) top the list of near-term investment priorities, signaling that manufacturers are concentrating on core shop-floor coordination and schedule reliability.

This prioritization reflects current operating pressures: labor constraints, demand volatility, and margin compression all place strain on planning accuracy and execution discipline. Strengthening planning and MES capabilities offers relatively fast, measurable returns — improved throughput, better schedule adherence, and reduced firefighting.

Company size again shapes investment focus. Firms with 200 or fewer employees are prioritizing production planning and scheduling, suggesting that smaller manufacturers are targeting foundational coordination capabilities. In contrast, companies with 500+ employees are concentrating on manufacturing execution and inventory management, reflecting the greater complexity of multi-line, multi-site, or multi-channel operations.

Industry variation reinforces the importance of sector dynamics. Electronics, food & beverage, and aerospace/automotive/defense lead in production planning investments — industries characterized by high variability, regulatory oversight, or tight customer delivery expectations. Inventory management investment is heavily concentrated in food & beverage and fabrication, likely driven by perishability, working capital pressure, and material cost volatility. Electronics leads quality management investment, reflecting defect sensitivity and product lifecycle compression. Meanwhile, raw materials sectors prioritize warehousing and logistics, highlighting the importance of flow efficiency and material movement in upstream supply chains.

Collectively, the data suggests that manufacturers are directing capital toward operational control points — areas where improved coordination directly translates to performance stability.

Forward-Looking Implications

- Execution excellence will dominate the next 12–24 months.

Manufacturers are prioritizing initiatives that stabilize core operations rather than pursuing transformational overhauls. This indicates a pragmatic investment mindset shaped by economic uncertainty. - Planning accuracy will become a central competitive lever.

As volatility persists, companies that can dynamically adjust schedules, balance capacity, and align inventory with demand will outperform slower, spreadsheet-driven operations. - Inventory optimization remains a working capital priority.

With supply chain variability still present, investments in inventory visibility and control will continue to attract funding — particularly in sectors with high material cost exposure. - Quality and compliance digitization will intensify in high-precision sectors.

Electronics and aerospace/automotive/defense may accelerate investments in digital quality systems as regulatory scrutiny and customer standards rise. - Investment sequencing will matter more than scale.

Organizations that align digital investments with their most acute operational constraints — rather than industry trends — will realize faster returns and stronger internal buy-in.

Overall, the near-term digital roadmap across manufacturing reflects disciplined prioritization. Rather than chasing innovation headlines, companies are concentrating on the operational backbone: planning, execution, inventory, quality, and logistics. Those that strengthen these foundational capabilities will be better positioned to layer advanced analytics and automation in subsequent phases of transformation.

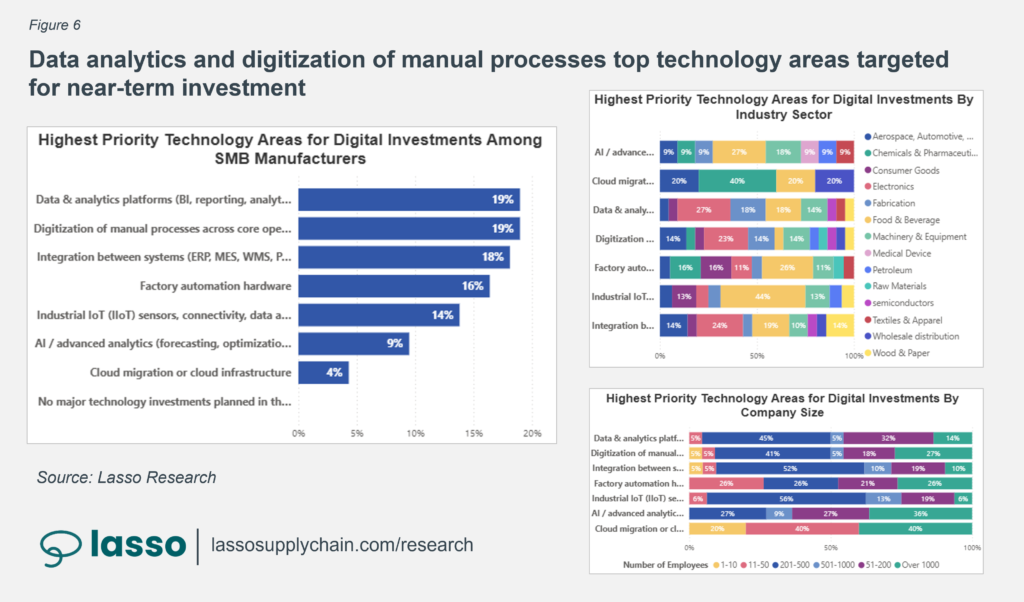

Highest priority near-term technology investment areas

In an environment defined by rapid technological advancement and constrained capital allocation, manufacturers are sharpening their focus on the technologies most likely to deliver immediate strategic value. Rather than pursuing broad digital overhauls, leadership teams are concentrating near-term investments on platforms and tools that strengthen data infrastructure, enhance automation, improve connectivity, and enable advanced analytics. Decisions are increasingly guided by scalability, integration capability, cybersecurity resilience, and speed to measurable ROI. This section outlines the technology categories manufacturers rank as their highest near-term investment priorities, providing insight into where budgets are being directed and how organizations are positioning themselves for the next phase of digital competitiveness.

Insights at a Glance: Near-Term Digital Technology Investment Areas

- Data Analytics and digitization of manual processes were the top selections among respondents, each with 19%.

- Both Data Analytics and Digitization of manual processes were primarily driven by companies with between 50-500 employees.

- For Factory Automation Hardware, 74% were from companies with more than 50 employees.

- Among companies with less than 50 employees, Factory Automation Hardware and Migration to Cloud infrastructure were the top near-term technology investment areas.

- The most frequently cited industries making near-term data analytics investments were Electronics, Fabrication, Machinery Equipment, and Food & Beverage.

- The most frequently cited industries making near-term manual process digitization investments were Electronics, Machinery Equipment, and Aerospace/Automotive/Defense.

Manufacturers are prioritizing analytics and process digitization as scalable, near-term enablers of operational control and competitiveness.

The data reflects a pragmatic and infrastructure-focused investment mindset. Data analytics and digitization of manual processes, each cited by 19% of respondents, top the list of near-term technology priorities. This suggests that many manufacturers recognize the need to first strengthen their data foundation and eliminate workflow friction before advancing to more complex automation or AI-driven capabilities.

Notably, both priorities are primarily driven by mid-sized organizations (50–500 employees). This segment often sits at a pivotal inflection point: complex enough to outgrow spreadsheets and manual coordination, but still agile enough to modernize systems without the inertia of very large enterprises.

Factory automation hardware shows a different adoption pattern. While 74% of those prioritizing automation hardware have more than 50 employees, smaller firms (under 50 employees) rank factory automation and cloud migration as their top technology investments. For these smaller organizations, automation may directly address labor constraints, while cloud infrastructure offers scalable IT capability without heavy internal overhead.

Industry patterns further highlight sector-specific drivers. Electronics, fabrication, machinery equipment, and food & beverage are leading in analytics investment — industries where variability, traceability, and margin sensitivity heighten the value of data-driven decision-making. Manual process digitization is especially prominent in electronics, machinery equipment, and aerospace/automotive/defense, where compliance requirements, engineering complexity, and quality documentation demands increase the cost of paper-based workflows.

Overall, manufacturers appear to be prioritizing technologies that improve data accessibility, workflow consistency, and decision velocity — foundational capabilities that support broader digital maturity.

Forward-Looking Implications

- Data infrastructure will precede advanced intelligence.

The emphasis on analytics and digitization indicates that organizations understand predictive and AI-driven initiatives require clean, connected, and standardized data environments first. - Mid-market manufacturers are entering acceleration mode.

The 50–500 employee segment may drive the next wave of digital advancement, as they invest aggressively in analytics and workflow modernization to compete with larger enterprises. - Automation investment will increasingly align with labor strategy.

As workforce shortages persist, factory automation hardware will continue to gain traction — particularly among firms seeking resilience against skilled labor constraints. - Cloud adoption will enable scalability for smaller firms.

Cloud migration among sub-50 employee companies suggests a recognition that flexible infrastructure is essential for future growth and cybersecurity resilience. - Industry complexity will dictate technology sequencing.

Highly regulated and high-mix industries will likely continue leading investments in digitization and analytics, while capital-intensive sectors may balance software investment with physical automation.

In summary, near-term technology priorities signal a disciplined approach to digital competitiveness. Manufacturers are investing in scalable, integrative technologies that strengthen their operational backbone — setting the stage for more advanced automation, predictive analytics, and AI-driven optimization in the next phase of transformation.

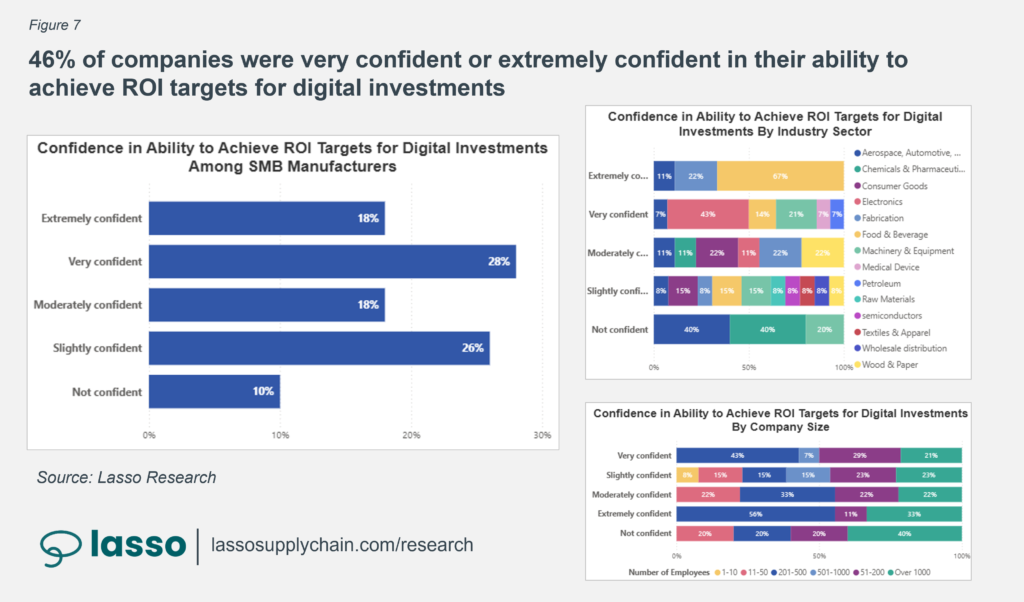

Confidence in ability to achieve ROI from digital investments

As digital spending continues to rise across manufacturing and supply chain operations, executive confidence in achieving measurable returns has become a critical leading indicator of future investment behavior. While many organizations recognize the strategic necessity of modernization, confidence levels vary based on past implementation success, internal capabilities, data maturity, and alignment between technology initiatives and operational objectives. Some manufacturers report strong conviction in their ability to translate digital initiatives into cost savings, productivity gains, and margin improvement, while others remain cautious due to integration complexity, change management challenges, or unclear performance benchmarks. This section examines how confident manufacturers are in realizing ROI from digital investments—and what differentiates high-confidence organizations from their more uncertain peers.

Insights at a Glance: Future ROI Confidence

- 46% of companies were very confident in their ability to achieve ROI targets for digital investments while 36% were partially confident or not confident.

- Among companies partially confident or not confident, 44% were companies with 50 or fewer employees.

- Among companies that were very confident in their ability to achieve ROI targets on digital manufacturing investments, 71% were companies with over 200 employees.

- Among respondents that were very confident in their ability to hit ROI targets, 63% were from the Electronics or Machinery Equipment sectors.

- Among respondents that were not confident, 80% were from the chemicals or Aerospace/automotive/defense sectors.

Confidence in digital ROI is polarized, with scale and sector maturity strongly influencing outlook.

The data reveals a manufacturing sector split between conviction and caution. While 46% of companies report being very confident in their ability to achieve ROI targets from digital investments, more than one-third (36%) remain partially confident or not confident. This level of uncertainty signals that digital transformation is still perceived as execution-sensitive rather than guaranteed value creation.

Company size is one of the strongest differentiators. Among those lacking confidence, 44% are firms with 50 or fewer employees — organizations that may face resource constraints, limited internal expertise, or prior implementation challenges. In contrast, 71% of companies that report being very confident have over 200 employees. Larger firms likely benefit from structured implementation processes, clearer KPIs, prior transformation experience, and dedicated digital leadership.

Industry concentration further sharpens the divide. Electronics and machinery equipment sectors account for 63% of the very confident respondents. These industries may have more standardized processes, stronger engineering cultures, or clearer digital use cases tied directly to quality and throughput. Conversely, 80% of respondents who report low confidence are concentrated in chemicals and aerospace/automotive/defense. These sectors often face complex regulatory environments, capital intensity, long validation cycles, or integration challenges that can complicate ROI realization timelines.

Importantly, confidence does not necessarily correlate perfectly with digital adoption levels. Instead, it appears tied to organizational capability — including governance, change management, data maturity, and execution discipline.

Forward-Looking Implications

- Confidence will shape future investment velocity.

Organizations with strong ROI conviction are more likely to accelerate digital spending, compounding their maturity advantage. Those with lower confidence may delay or narrow investments, potentially widening the competitive gap. - SMB enablement will be critical to sustaining sector-wide momentum.

Smaller firms’ lower confidence levels suggest a need for clearer implementation roadmaps, phased investment strategies, and measurable early wins to build internal belief in digital returns. - Industry complexity influences perceived risk.

Highly regulated or capital-intensive sectors may require longer ROI horizons and more rigorous validation frameworks. Tailored performance metrics and realistic time-to-value expectations will be key. - Execution maturity will become the defining capability.

As technology becomes more accessible, differentiation will shift toward governance models, leadership alignment, and cross-functional adoption — the elements that convert digital intent into measurable results. - Transparency in ROI measurement will increase.

Organizations will likely formalize ROI tracking mechanisms, linking digital initiatives directly to cost, throughput, working capital, and margin metrics to reinforce confidence at the executive level.

In summary, while nearly half of manufacturers express strong confidence in achieving digital ROI, a significant share remains cautious. The dividing line appears less about technology access and more about organizational readiness and execution maturity. Over the next several years, building internal confidence may prove just as important as selecting the right technologies.

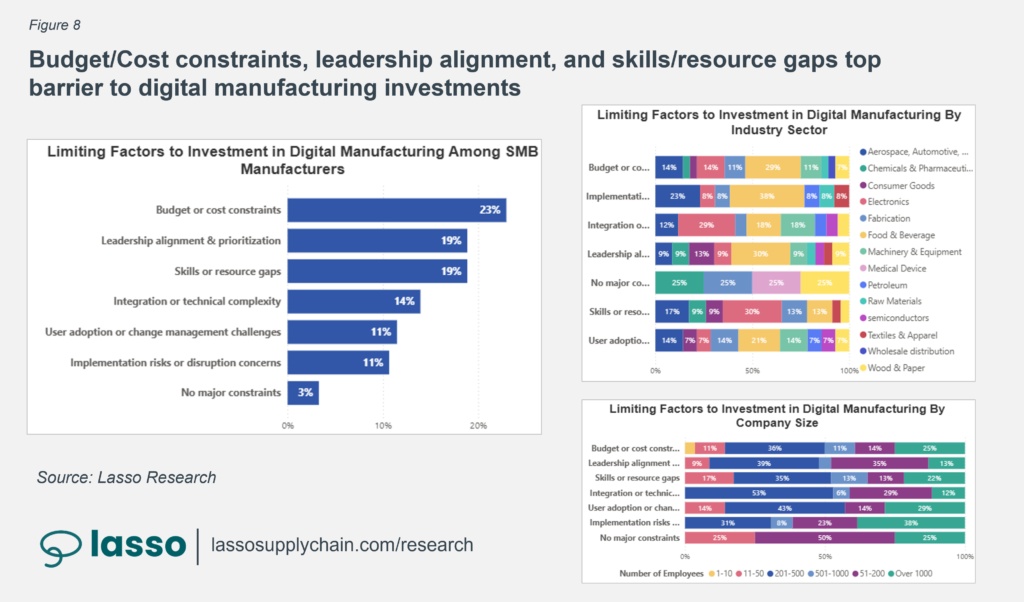

Barriers to digital manufacturing initiatives

Despite widespread recognition of the strategic importance of digital transformation, many manufacturing organizations continue to face significant obstacles in executing digital initiatives at scale. Financial constraints, legacy systems, data silos, cybersecurity concerns, and workforce skill gaps frequently slow progress or limit the scope of implementation. In addition, competing operational priorities and uncertain ROI projections can create hesitation at the leadership level. This section explores the most common barriers manufacturers encounter when pursuing digital manufacturing initiatives, examining both structural and organizational challenges that influence adoption speed, investment confidence, and long-term success.

Insights at a Glance: Barriers to Digital Manufacturing Initiatives

- Budget & Cost contrainst was the top barrier to digital manufacturing investments cited 23% of the time while Leadership alignment and skills/resource gaps were the next highest, cited 19% each.

- The lowest cited barrier was implementation/disruption risk and user adoption challenges.

- Among those that cited leadership alignment as the biggest challenge, 91% had more than 50 employees.

- Among companies with 10 or fewer employees, 100% of the top barriers were budget/cost constraints.

- Among companies with over 1000 employees, the top concern after budget constraints was the implementation and disruption risk.

- Among the Electronics, Aerospace, and Fabrication sectors, the biggest barriers were Skills gaps and budget constraints.

- The sectors most frequently citing challenges with leadership prioritization were Consumer Goods and Chemicals sectors.

Cost pressures, leadership alignment, and capability gaps—not technology—are the primary barriers to digital progress.

The findings make clear that digital transformation in manufacturing is constrained less by awareness and more by execution realities. Budget and cost constraints emerge as the most frequently cited barrier (23%), reinforcing that capital allocation discipline remains tight, particularly in uncertain economic conditions.

However, financial limitations tell only part of the story. Leadership alignment and skills/resource gaps follow closely behind (19% each), signaling that organizational readiness is equally influential. Digital initiatives often require cross-functional coordination, new governance models, and operational change — areas where misalignment can stall momentum even when funding is available.

Company size introduces further nuance. Among firms with 10 or fewer employees, budget constraints account for 100% of top-cited barriers, highlighting the stark capital limitations facing very small manufacturers. For larger organizations, barriers become more structural. Among those citing leadership alignment as the biggest challenge, 91% have more than 50 employees — suggesting that complexity increases with scale. Meanwhile, companies with over 1,000 employees identify implementation and disruption risk as a major secondary concern, reflecting the operational stakes involved in large-scale system changes.

Industry patterns also underscore capability-driven challenges. Electronics, aerospace, and fabrication sectors most frequently cite skills gaps and budget constraints — industries that often require specialized technical expertise and high integration rigor. Consumer goods and chemicals sectors report leadership prioritization challenges more frequently, indicating potential strategic hesitation or competing transformation agendas.

Interestingly, implementation disruption and user adoption challenges rank among the lowest cited barriers overall. This may suggest growing familiarity with digital deployments — or it may reflect that financial and leadership hurdles prevent projects from advancing far enough for adoption challenges to fully surface.

Forward-Looking Implications

- Financial discipline will remain a gating factor.

As ROI expectations rise, digital initiatives will increasingly need clear business cases, phased funding models, and measurable milestones to secure approval. - Organizational alignment will determine transformation speed.

Leadership cohesion and clearly defined digital ownership structures will become decisive differentiators, particularly in mid-sized and large enterprises. - Talent strategy will be central to sustained progress.

Skills gaps across analytics, systems integration, and change management suggest that workforce development and external partnerships will be critical accelerators. - Scale amplifies complexity risk.

Large enterprises must balance transformation ambition with operational continuity, emphasizing structured rollout strategies and risk mitigation frameworks. - Smaller firms need capital-efficient pathways.

For very small manufacturers, modular technologies, subscription models, and incremental automation may offer more realistic entry points into digital modernization.

In summary, the barriers to digital manufacturing initiatives are primarily organizational and economic rather than technological. The tools exist, and awareness is high. The next wave of digital progress will depend on how effectively manufacturers align leadership, allocate capital, and build internal capabilities to move from intention to sustained execution.

Turning Insight into Action

Digital transformation in manufacturing is no longer defined by ambitious technology roadmaps alone—it is increasingly measured by the ability to translate data into better operational decisions. Across the findings in this report, a clear pattern emerges: manufacturers that prioritize practical, targeted digital initiatives are seeing measurable improvements in visibility, efficiency, and financial performance.

For many small and mid-sized manufacturers, the most impactful progress does not come from sweeping, enterprise-wide programs. Instead, it comes from focused investments that address specific operational challenges—improving inventory visibility, reducing scrap, strengthening supplier performance, or gaining clearer insight into job-level profitability. When these initiatives are supported by reliable data and accessible analytics, they enable teams across the organization to make faster, more confident decisions.

At the same time, the barriers identified in this research highlight an important reality: successful digital initiatives depend as much on organizational alignment and execution as they do on technology itself. Companies that invest in the right capabilities—data infrastructure, analytics expertise, and cross-functional collaboration—are better positioned to realize the full value of their digital investments.

As competitive pressures continue to grow and operational complexity increases, the ability to leverage data effectively will become an increasingly important differentiator. Manufacturers that build strong analytics foundations today will be better equipped to improve operational performance, respond to changing market conditions, and sustain long-term growth.

Practical insights. Clear visibility. Better manufacturing decisions.

Lasso is a data analytics consulting firm that helps small and mid-sized manufacturers turn their data into a competitive advantage.

We work closely with manufacturing leaders to uncover the insights hidden inside operational data—from ERP systems and shop-floor processes to supply chains and financial performance. Our focus is simple: deliver clear, actionable analytics that improve decision-making, strengthen margins, and drive measurable operational improvements.

By combining deep data expertise with a practical understanding of manufacturing operations, we help organizations move beyond spreadsheets and fragmented reporting to build reliable analytics foundations. The result is better visibility into costs, inventory, production performance, and profitability—enabling teams to operate more efficiently and compete with confidence in increasingly complex markets.